Well, what a year we’ve had! As 2023 winds up, we are glad to see her in the rear view mirror! 2024 should bring lower rates and more inventory for home buyers to choose from!

MARKET AND RATES

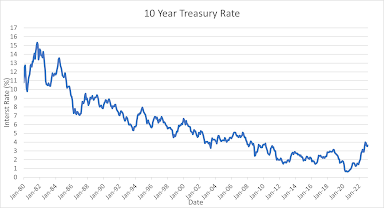

While the volume of home sales hit a record low this year,

prices have continued to rise in most of Southern California. If you are planning a home purchase, we

strongly recommend that you move sooner than later. We will experience a buying frenzy as

soon as rates get a bit lower (they have already softened in the last month)

and buyers will come off the sidelines in droves. With lower rates, more homeowners will list

their homes. One might think more homes

on the market would mean prices will drop.

But, there is so much pent up demand there is no indication that home

prices will come down. Don’t delay!

A REAL STORY

In the last week, two different clients called us, ready to

make an offer on a property. They had

gone to an open house, and loved the home.

However, in both cases, they were not yet pre-approved. We had not had time to collect data and

strategize with them. By the time they

provided us the documentation required (income and asset information primarily)

so we could pull a credit report and run automated underwriting, the home was

already in escrow and pending close. Get

Pre-Approved ahead of time! Don’t

delay and miss out on your dream home!

We work with some buyers over a year to prep ahead of time.

GOOD NEWS FOR 2-4 UNITS

Until last month, buyers or owners of 2-4 units needed to

have a minimum of 15% down or more. The

Agencies (FNMA and FREDDIE) have reduced the minimum down payment required for

2-4 unit properties to 5%, so long as one of the units is owner-occupied. This is fabulous news. Remember, you will receive credit for 75% of

the imputed rental income for the other units, so this actually helps qualify

for a purchase!!

NEW INCREASED CONFORMING LOAN LIMITS

Conforming loans meet FNMA and FHLMC guidelines. These guidelines are more lenient vs. Jumbo

loan programs, so the rise in the loan limits is good news. Many counties throughout California have

different loan limits-- so we always need to check, depending on property

address.

$1,149,825 – LA and Orange County; San Diego is slightly

lower.

$766,550 – Riverside and San Bernardino

TAX RETURN REMINDER

Please don’t file your federal returns for 2023 until we can

review them, if you plan to buy or refi next year. This can make or break a successful

transaction.

MERRY CHRISTMAS and HAPPY HANNUKAH TO ALL. REMEMBER TO BE SAFE, BE KIND, AND CHERISH YOUR LOVED ONES. WE LOST A DEAR FRIEND THIS MONTH.

As always call us with any questions or concerns you may

have.